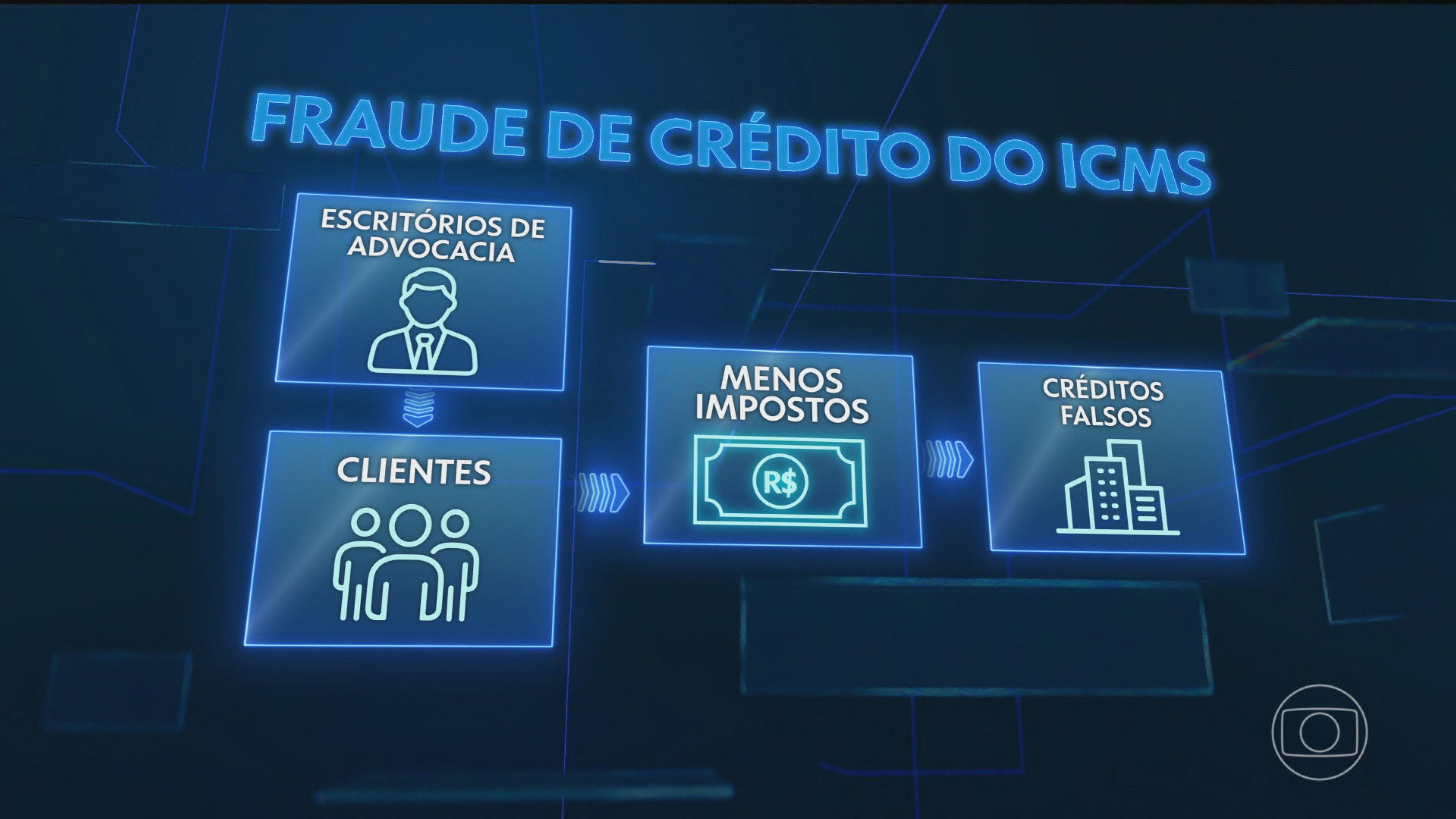

Law Firms Suspected of R$3.8 Billion ICMS Tax Fraud in São Paulo

A joint operation involving the Public Prosecutor's Office, police, and the São Paulo State Finance Secretariat has targeted law firms suspected of orchestrating a massive tax evasion scheme. The investigation focuses on the fraudulent sale of fake ICMS (Value Added Tax on Sales and Services) credits, potentially amounting to R$3.8 billion, with estimates suggesting the total fraud could reach R$4 billion. ICMS credits are generated when companies pay the tax on purchased inputs, which can then be deducted from the ICMS owed on sales. Companies involved in interstate sales or exports can accumulate these credits, which, after authorization, can be transferred to other businesses. Investigators allege that law firms exploited this mechanism by offering clients the opportunity to reduce their tax burden by purchasing fake ICMS credits from non-existent or bankrupt companies. These firms allegedly fabricated credits, guarantees, and even simulated meetings with tax auditors to deceive clients. As a result, numerous companies drastically reduced their tax payments to the state, with some paying as little as R$100,000 on liabilities that were previously around R$1 million to R$2 million. The task force identified suspicious transactions from 870 companies, leading to 38 search and seizure warrants executed across six cities in São Paulo and Paraná. Among those investigated is Nelson Wilians, owner of a major Brazilian law firm, who was previously investigated for INSS fraud. His wife, Anne Wilians, a partner in the firm, is also implicated. Authorities believe similar fraud schemes may be occurring nationwide, potentially causing billions in losses to other states.

This investigation into alleged ICMS credit fraud highlights systemic vulnerabilities in tax credit transfer mechanisms, particularly when facilitated by intermediaries like law firms. The scale of the alleged fraud, nearing R$4 billion, suggests potential gaps in regulatory oversight and the need for enhanced due diligence protocols for inter-company credit transactions. The involvement of established legal entities raises questions about internal compliance structures and the ethical responsibilities of professional service providers. Future reforms might consider stricter auditing requirements for credit transfers, greater transparency in the credit market, and potentially the use of blockchain technology to create immutable records of tax credit transactions, thereby mitigating the risk of counterfeit credits and ensuring greater accountability within the tax system.

AI-generated to prompt reflection — not editorial opinion, not advice, not a statement of fact. How this works.